Insights on financial literacy campaigns that empower communities

Engaging different demographics in financial education involves tailoring content and methods to meet unique needs, utilizing community leaders, and ensuring accessibility through diverse formats to promote financial literacy effectively.

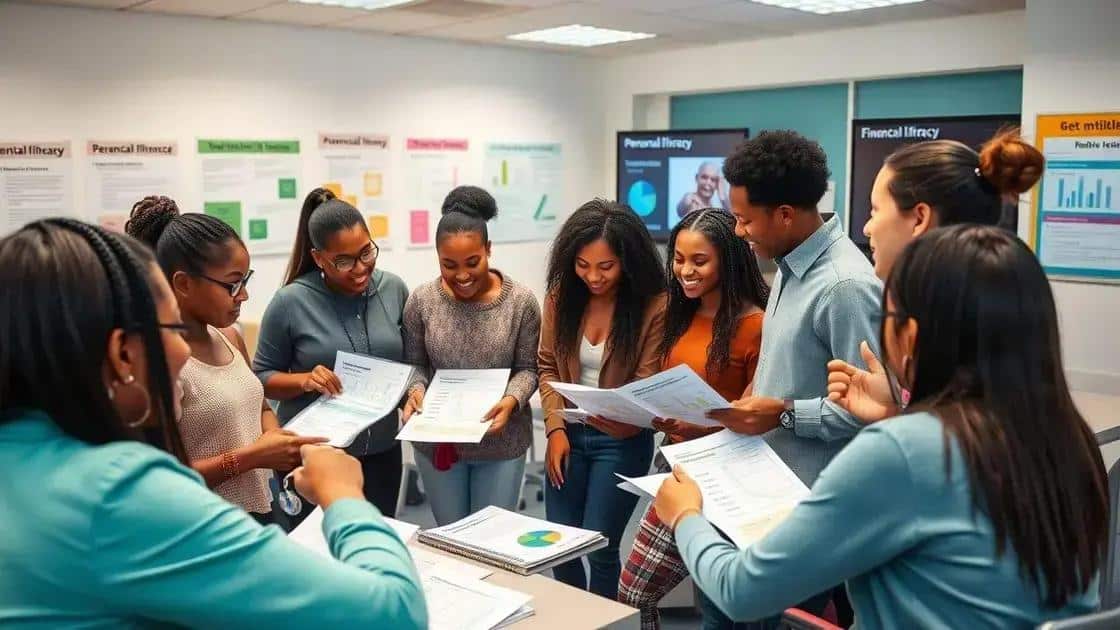

Insights on financial literacy campaigns highlight their importance in shaping confident and informed financial decision-makers. Have you ever wondered how effective strategies can transform individuals’ financial futures? This article dives into pivotal approaches and impacts of these campaigns.

Understanding financial literacy campaigns

Understanding financial literacy campaigns is crucial for helping individuals manage their finances effectively. These campaigns can change lives by providing the knowledge needed to make sound financial decisions.

What are financial literacy campaigns?

Financial literacy campaigns aim to educate people about money management. They offer resources to help individuals understand budgeting, saving, and investing. By simplifying complex financial concepts, these campaigns make personal finance accessible for everyone.

- Target diverse audiences to ensure inclusivity.

- Utilize various platforms like workshops, social media, and seminars.

- Create easy-to-understand materials that resonate with everyday experiences.

Understanding your audience is essential. Every campaign should focus on specific demographics. Knowing whether you’re addressing students, families, or seniors can shape the campaign’s tone and content. Providing tailored content enhances the effectiveness of your initiatives.

Key elements of successful campaigns

Successful financial literacy campaigns often include interactive components. These can engage participants better and create lasting knowledge. For instance, quizzes and discussions encourage active learning.

- Incorporate real-life examples that illustrate concepts.

- Provide step-by-step guidance for common financial tasks.

- Foster a community atmosphere for participants to share experiences.

Monitoring the outcomes of these campaigns is vital. Gathering feedback helps in refining future efforts and measuring success. Additionally, sharing success stories can inspire others to join financial literacy programs.

Key strategies for successful campaigns

Key strategies for successful campaigns play a vital role in how effectively information reaches and influences individuals. With careful planning and execution, these strategies can transform educational initiatives into impactful movements.

Identify your target audience

Knowing who you are trying to reach is crucial. Different age groups and demographics will have unique financial needs and learning preferences. Tailoring your message to speak directly to these groups makes it more relatable.

- Conduct surveys to gather data on financial literacy levels.

- Engage community leaders to understand specific needs.

- Design content that resonates with various demographics.

Creating engaging content is essential. Utilize formats such as videos, infographics, and interactive workshops to keep participants interested. This variety helps in accommodating different learning styles, ensuring that everyone can absorb the information effectively.

Utilize partnerships for greater reach

Collaborating with local organizations can amplify your efforts. Establishing partnerships with schools, nonprofits, and businesses can lead to increased resources and visibility. When stakeholders work together, they can leverage each other’s strengths for a stronger campaign.

- Share resources to develop materials that are widely accessible.

- Host joint events that draw larger audiences.

- Cross-promote initiatives through social media channels.

Regularly evaluating the impact of your campaign is key. Tracking progress helps identify what works and what needs adjustment. Use metrics such as participant feedback and changes in financial behavior to measure success and refine future projects.

Measuring the impact of financial literacy

Measuring the impact of financial literacy is essential to understanding how effective campaigns can be. It helps identify what methods work best and where improvements are needed. Without proper measurement, it is difficult to gauge the success of educational initiatives.

Defining clear goals

Before measuring impact, it is crucial to set specific and measurable goals. These goals should focus on what knowledge or skills participants should gain. For instance, aiming to increase the percentage of people who create a budget after participating in a program can provide a clear benchmark.

- Establish baseline data to compare future results.

- Set achievable objectives to track progress.

- Focus on both short-term and long-term outcomes.

Collecting data is an ongoing process. Surveys and assessments can be tools to gather feedback from participants. These can help in understanding not only what they learned but also how they apply that knowledge in real life. Regularly collecting this information allows for timely adjustments to the program.

Analyzing participant behavior

Tracking changes in participants’ financial behavior is vital. This can include monitoring changes in saving habits, investment knowledge, or overall financial confidence. For instance, increased engagement in savings accounts or better credit management are signs of positive impacts from literacy campaigns.

- Use pre-and post-program surveys to assess knowledge gain.

- Evaluate behavioral changes over time through follow-ups.

- Analyze qualitative feedback for deeper insights.

Additionally, sharing success stories can amplify the message. When participants share how their lives have changed due to financial education, it encourages others to engage in similar programs. This not only showcases impact but also builds community interest.

Engaging different demographics in financial education

Engaging different demographics in financial education is essential to ensure everyone benefits from financial literacy. Each group has unique needs, which require tailored approaches to increase participation and comprehension.

Understanding demographic differences

Demographics such as age, income level, and educational background influence how financial information is received. For instance, younger audiences may prefer digital platforms, while older adults might benefit more from face-to-face workshops. Recognizing these differences is the first step to effective engagement.

- Analyze the preferred communication styles of each demographic.

- Offer content in multiple formats, like videos, brochures, and online courses.

- Adapt teaching methods to suit various learning preferences.

Building trust within communities is also vital. Many individuals may feel hesitant to engage with financial information due to past experiences or cultural barriers. Offering community-specific programs that resonate with participants fosters a supportive environment.

Utilizing community leaders

Community leaders can play a crucial role in promoting financial education. They can help bridge gaps by advocating for programs and encouraging participation. Collaborating with trusted figures can lead to greater acceptance and attendance in financial workshops.

- Invite local leaders to co-host workshops.

- Use their platforms to spread awareness about financial literacy goals.

- Highlight the importance of financial education through community events.

Engagement strategies such as gamification can also enhance participation. Fun activities that incorporate financial concepts can make learning enjoyable. For example, using competitions or challenges can motivate individuals to improve their financial skills.

FAQ – Frequently Asked Questions about Engaging Different Demographics in Financial Education

Why is it important to engage different demographics in financial education?

Engaging different demographics ensures that everyone has access to financial literacy, which helps build a more financially informed community.

What methods can be used to reach young audiences?

Utilizing digital platforms like social media and interactive apps can help engage younger audiences effectively.

How can community leaders contribute to financial education initiatives?

Community leaders can promote programs, build trust, and encourage participation by using their influence and credibility.

What role does content variety play in financial education?

Offering content in various formats, such as videos, workshops, and online courses, helps cater to different learning styles and keeps participants engaged.